US Stocks' Upside Outlier Performance in 2023 Looks Vulnerable

American equities have enjoyed a hefty return premium for much of this year relative to the rest of the major asset classes, but in the current environment that outlier performance looks increasingly vulnerable.

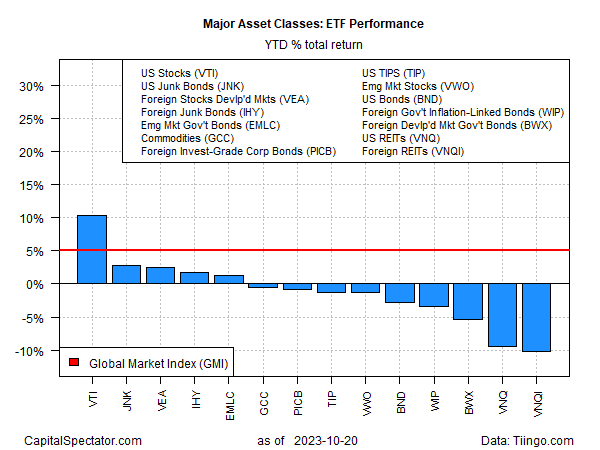

US equities are still leading global markets by a wide margin, based on a set of proxy ETFs through Friday’s close (Oct. 20). Vanguard Total US Stock Market Index Fund (VTI), despite recent losses, is up 10.3%. Although that’s roughly half the year-to-date gain vs. the scorecard for VTI at the end of July, in relative terms it still represents a hefty edge over the competition.

The second-strongest performer this year: US junk bonds (JNK), up a relatively moderate 2.8%. Note, too, that the majority of the major asset classes are now in the red for 2023. The deepest cut: property shares ex-US via Vanguard Global ex-U.S. Real Estate Index Fund (VNQI), which has lost more than 10% through Friday’s close.

The main headwind at the moment: rising Treasury yields. In early trading today, the US 10-year yield rose above 5%, marking the highest level since 2007. Higher yields present investors with increasingly competitive alternatives to stocks, which previously benefited from near-zero yields.

“The best combination of risk and return is to lock in higher interest rates for longer,” says Lawrence Gillum, chief fixed income strategist at LPL Financial.

That’s getting easier because “the bond vigilante is coming back,” observes Kevin Zhao, head of global sovereign and currency at UBS Asset Management. The term “vigilante” refers to bond investors who view monetary or fiscal policy as inflationary and decide to sell bonds, which raises yields. “This is very important for asset prices in equity, house prices, fiscal policy, monetary policy, so no longer is this a free ride on bond markets anymore — so the government has to be very careful in terms of the future.”

For strategists assessing changes to asset allocation, the higher expected return for bonds (approximated with current yield) has increased. The competition for stocks, in other words, is no longer weak, as it was when yields were lower and in some cases virtually zero before the Federal Reserve began raising its target rate in March 2023.

The quasi state of market equilibrium, in short, has taken a hit lately as investors reassess expected return and risk. The change puts US stocks in the crosshairs, which are still enjoying outsized year-to-date returns.

Exactly how the recalibration in market expectations unfolds is uncertain, but for now the path of least resistance seems to be one of equalizing performance differences until more confidence about the future emerges.

“All moves higher in yield pose the same difficulties for the markets — a higher ‘risk-free’ rate will encourage investors to reduce riskier asset holdings like equities, credit and emerging market assets, and allocate more into Treasuries,” advises Peter Chatwell, head of global macro strategies trading at Mizuho International.