April 4, 2026 Market Update

Market Recap: A Recovery of Sorts.

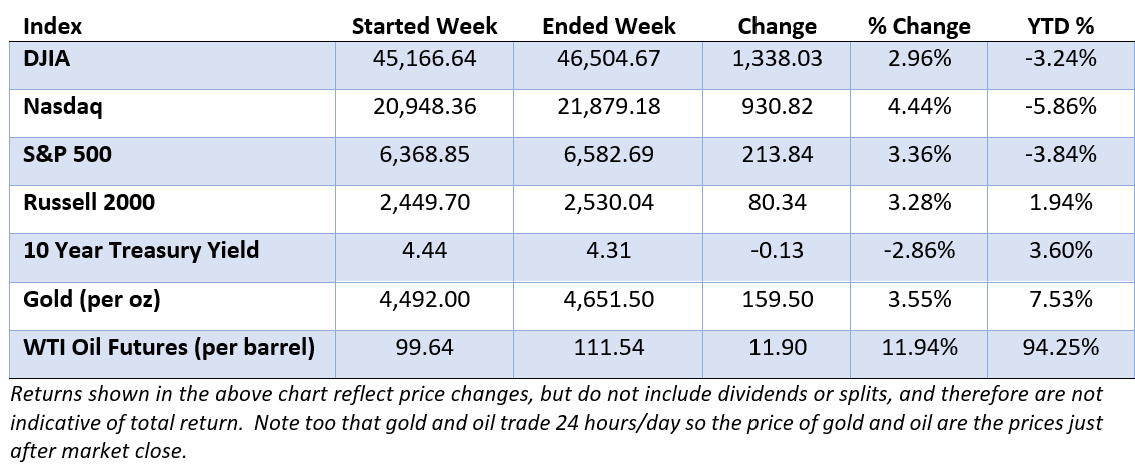

After weeks of selling pressure that pushed major indexes toward correction territory, stocks staged a powerful relief rally during the holiday-shortened trading week. The surge was primarily driven by headlines suggesting a potential diplomatic resolution to the conflict in Iran is close at hand. The news led to the S&P 500 reclaiming its 200-day moving average and posting its strongest two-day gain of the year on Tuesday and Wednesday.

"Higher for longer" remains the dominant theme for bond traders, despite the holiday-shortened week. Treasury yields remained elevated overall despite some late-week easing, as oil prices hovered near $110 per barrel, keeping inflation concerns front and center. Bond traders still seem to be expecting the Federal Reserve to sit tight for now, while the traditional "flight to safety" into government bonds has yet to materialize in a meaningful way.

Looking ahead to the start of the second quarter, the rotation away from high-valuation growth names and into cyclical, inflation-resistant sectors like energy and materials continues. While the late-quarter rally provided a boost for diversified portfolios, April will likely be directed by whether corporate earnings can continue to support the stock market’s lofty valuations in the face of rising energy and debt costs.

Market Performance

Market Commentary: Markets On Edge.

Markets closed out a volatile first quarter of 2026 on Tuesday, as a surge in oil prices and disruptions to key commodity supply chains tied to the Iran conflict stoked concerns about inflation, pressured corporate profits and reduced the likelihood of near-term Federal Reserve rate cuts.

Looking back, equity markets initially showed resilience, with relatively modest declines at the onset of the conflict, reflecting expectations that tensions would be short-lived. However, selling pressure intensified as the war dragged on, pushing both the Dow Jones Industrial Average and the tech-heavy Nasdaq Composite into correction territory. Stocks rallied on Tuesday, with the S&P 500 gaining nearly 3% in a single session and the Nasdaq rising close to 4%, following comments from President Trump that the conflict could be resolved within weeks.

Meanwhile, fixed income securities provided only limited diversification, as bond markets were driven less by geopolitical uncertainty itself and more by the impact of higher oil prices on the outlook for inflation. As a result, investors scaled back expectations for near-term Federal Reserve rate cuts, pushing Treasury yields higher and bond prices lower during the quarter.

News headlines often lead investors to question how their portfolios are positioned. But history suggests that the greatest risk is often not the volatility driven by those headlines, but the decisions investors make in response to it. Time and again, sharp market declines have been followed by strong recoveries—rewarding those who remained disciplined when uncertainty was at its peak.

In Case You Missed It: Closing In On A $1 Trillion.

OpenAI is now valued at $852 billion after securing $122 billion in new funding, the largest private financing deal in Silicon Valley history, highlighting continued investor appetite for artificial intelligence amid broader market volatility.