January 17, 2026 Market Update

Market Recap: So Far, So Good

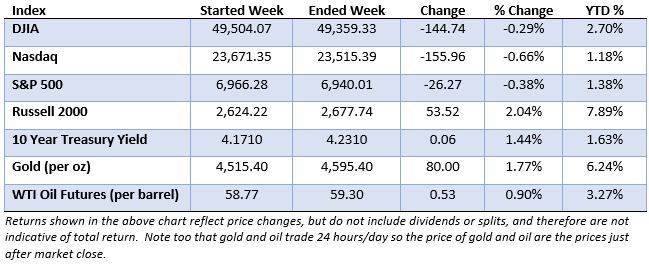

U.S. equity markets finished the second week of the new trading year with modest losses. Shares of regional banks and several industrial companies ended higher supported by generally strong earnings while shares of JPMorgan Chase, Citigroup, Bank of America, and Wells Fargo sharply declined after earnings reports raised concerns about credit conditions and margin pressure.

In the bond market, Treasury yields reversed course in the final trading sessions after declining for most of the week as investors responded to signs of easing inflation pressures and growing expectations for additional interest-rate cuts later this year. Markets also continued to digest the January 9th announcement that Fannie Mae and Freddie Mac have been directed to buy up to $200 billion in mortgage-backed securities, a move intended to help stabilize mortgage markets and support housing affordability. Meanwhile, corporate bond issuance reached roughly $88 billion this week alone, one of the largest weekly totals since 2020.

Looking ahead, Mr. Market will likely turn its attention to upcoming technology sector earnings next week. Given the sector’s heavy weighting in major market indexes, these reports could offer valuable insight into the outlook for the entire equity market for the balance of the year.

Market Performance

Market Commentary: Gimme Shelter

Mortgage rates fell to 6.06% this week, a multiyear low, fueling optimism that the housing market may finally be turning a corner. Most national forecasts call for home sales to grow by 1–3% in 2026. Inventory levels are also expected to improve gradually as borrowing costs ease, encouraging more homeowners to give up their ultra-low pandemic-era rates for nicer digs.

Although inventory is still tight, price increases have been more measured. The market continues to benefit from stable employment, rising wages, and limited new construction. Demand remains strong in Midwestern states such as Wisconsin, which never experienced the same degree of pandemic-era excess seen in many coastal markets.

Other developments that could boost the housing market include:

- Recent bills like the Housing for the 21st Century Act aim to reduce construction barriers and expand credit access.

- Pressure being exerted on the Federal Reserve by the Trump Administration to lower interest rates further.

- A wave of younger buyers is entering peak household-formation years.

In short, after several years challenged by affordability challenges, limited inventory, and elevated mortgage rates, the U.S. housing market appears to be entering 2026 on a more stable footing.

In Case You Missed It: First Homes Aren’t Starter Homes Anymore

According to recent Realtor.com and industry data, the typical first-time homebuyer in the U.S. is now 40 years old, up from about 33 years old just five years ago.