July 11, 2025 Market Update

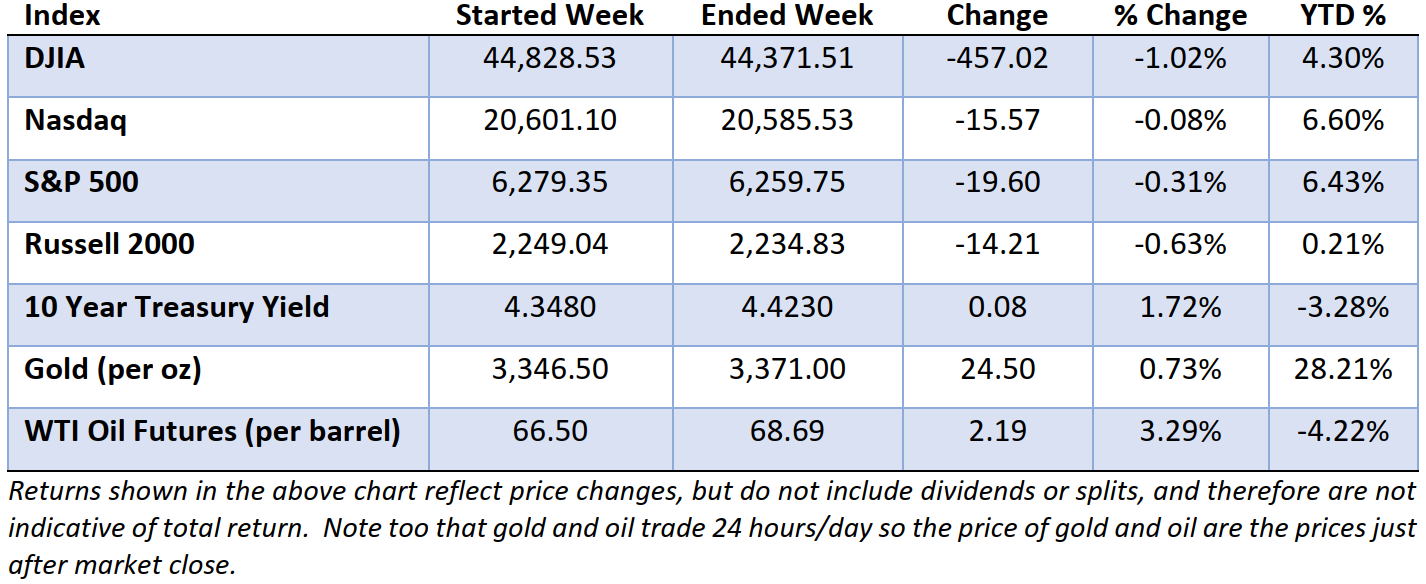

U.S. equities experienced a volatile week, initially reaching record highs midweek before retreating due to escalating trade tensions. President Trump's announcement of a 35% tariff on Canadian imports, effective August 1, sparked concerns over potential inflationary pressures and global economic repercussions. Despite these headwinds, the technology sector remained resilient, with Nvidia surpassing a $4 trillion market capitalization.

In the bond market, interest rates drifted higher this past week as concerns over inflationary implications of the newly announced tariffs took precedence over encouraging labor data and strong demand at a Treasury auction. Looking ahead, upcoming inflation readings and Fed commentary are likely to play a key role in determining the bond market’s direction.

Taken together, the week’s news reinforced the view that the economy remains on solid footing, but not without new challenges. While labor market strength supports the economic outlook, tariffs and inflation risks are rising. Accordingly, diversification and risk management are increasingly important in these unusual and uncertain times.

Mr. Market has entered the second half of the year with a surprisingly calm demeanor. Despite persistent uncertainty around interest rates, geopolitics, and global elections, equity volatility remains subdued and major indexes have trended sideways over the past few weeks.

The CBOE Volatility Index (VIX) continues to hover at low levels, and credit spreads have stayed tight—both signals of investor confidence and complacency. Even recent data surprises and policy ambiguity haven’t sparked major price swings, suggesting that markets are either highly resilient or unusually indifferent.

Historically, such periods of calm have often preceded sharper moves, particularly during transitions in monetary policy or earnings sentiment. With second-quarter earnings season kicking off and several central bank meetings on the horizon, catalysts for renewed volatility may be building beneath the surface.

Considerable research supports the idea that positive momentum can be a sound basis for tilting equity allocations toward sectors showing recent strength. However, investors should be cautious not to let the recent market calm encourage them to take that tilt too far, and to avoid overreacting if overweighted sectors experience a pullback while the tilt is in place.

That’s all for now. Have a great weekend and invest wisely my friends.