July 3, 2025, Market Update

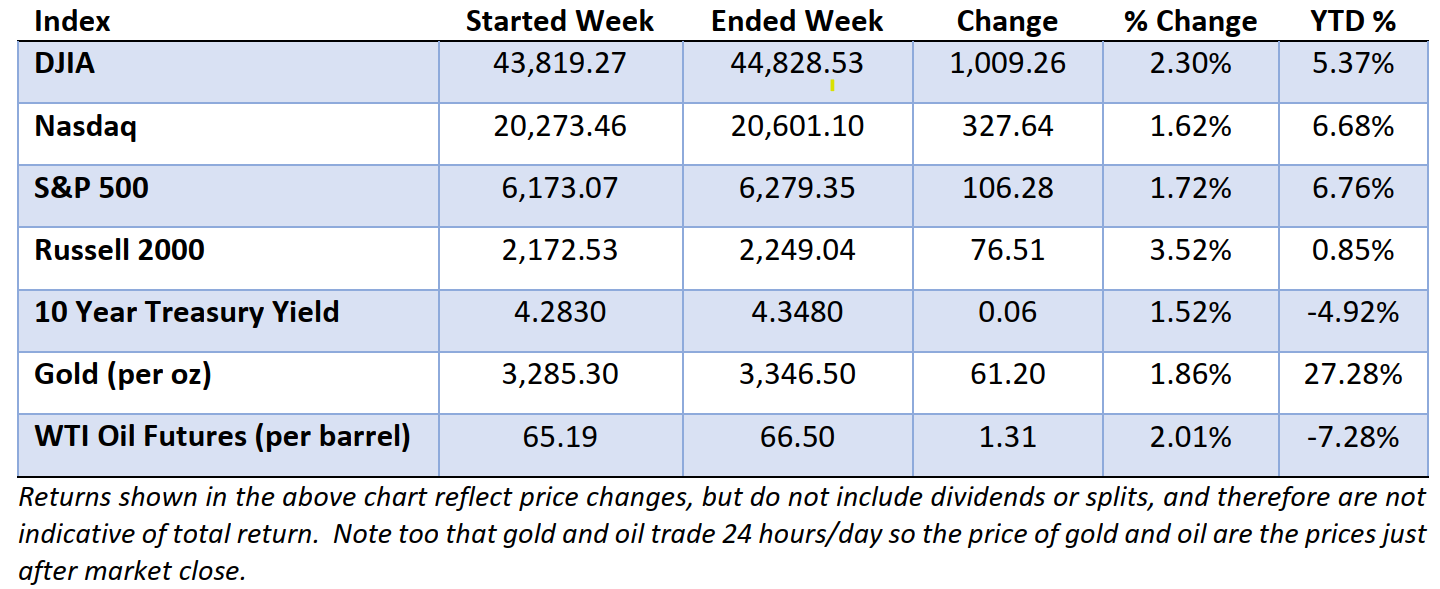

Stocks finished the holiday-shortened week on a positive note, with the major indexes posting solid gains. Small-cap stocks led the way, as the Russell 2000 rose more than 2% amid improving sentiment about the economic outlook following a series of encouraging data releases.

In the bond market, Treasury yields reversed course after climbing earlier in the week. A strong auction of new Treasurys on Wednesday helped support demand, and Thursday’s jobs report tempered expectations for near-term Fed rate cuts. Together, these factors helped keep long-term yields in check.

The June employment report showed a gain of 147,000 nonfarm payrolls—above expectations but still indicative of a gradual cooling from earlier in the year. Mr. Market interpreted the report as a sign that the economy stays resilient but is not at risk of overheating.

Stocks have been trading near all-time highs, with the S&P 500 up roughly 10% since former President Trump announced sweeping new tariffs on April 2, 2025. The gains have been driven by strong corporate earnings, positive economic data, and improving breadth, but much of the year’s advance is attributable to a handful of tech giants.

The stock market rally has sparked a familiar debate: are rising prices a sign of strength, or a reason for caution?

Historically, new highs are more common than investors might expect, and higher prices typically beget higher prices. But with expectations for large technology company future profits soaring—and their valuations soaring right along with them—the risk of disappointment is growing. The Wall Street Journal reports that as of last Monday, Nvidia shares have climbed 18% this year, Meta Platforms have gained 26%, and Microsoft has added 18%. Shares of data-analytics firm Palantir Technologies and chip maker Broadcom are up 80% and 19%, respectively.

In contrast, small-cap and value stocks have meaningfully lagged their large-cap growth counterparts this year. By comparison, international equities have posted strong gains, helped by a weaker dollar and recovering growth abroad.

In such market conditions, it’s patience that takes precedence. While the market’s positive momentum is encouraging, risks remain—especially around policy uncertainty and elevated valuations in key sectors. As a result, bold directional bets on where the market is headed over the next several months run the risk of backfiring.

That’s all for now. Have a great weekend—and invest wisely, my friends.