June 14, 2025 Market Update

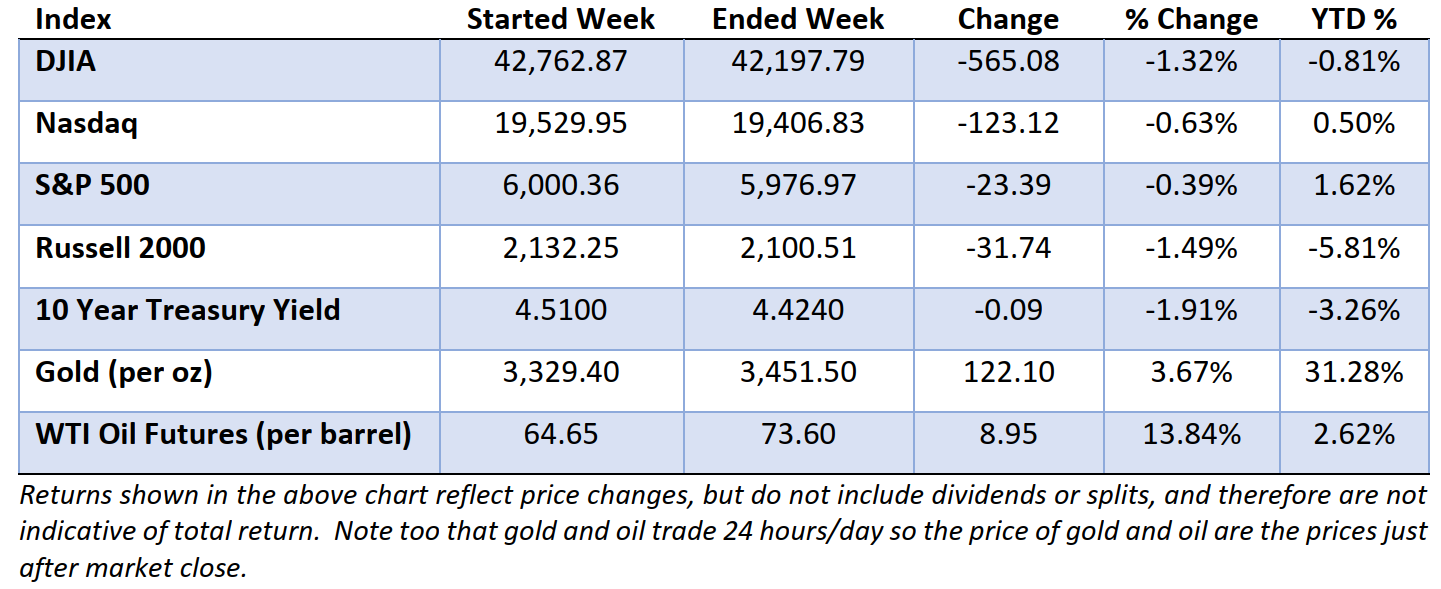

Stocks were on track for solid gains this past week, with the S&P 500 and the Nasdaq approaching their highs, as investors responded positively to a softer CPI report, strong earnings results, and a weaker dollar. Sentiment was further lifted by President Trump’s announcement of a tentative trade agreement with China, which added to hopes for improved global trade dynamics.

That optimism faded late Thursday and Friday on reports of an Israeli military strike on Iran followed by Iran’s retaliation. Oil prices jumped, gold rallied more than 1%, and the dollar strengthened as investors sought safe-haven assets amid rising geopolitical uncertainty.

Treasury yields fell across the curve, with the 2-year yield declining meaningfully in response to soft labor market data and a more cautious tone in the Fed’s latest meeting minutes. While recent trends had supported hopes for a soft landing, the question now is whether these favorable conditions can hold—and whether renewed geopolitical tensions will destabilize an otherwise improving outlook.

Last week offered a stark reminder of just how quickly investor sentiment can shift. Cooling inflation, a tentative trade deal with China, evolving expectations around Fed policy, and escalating geopolitical tensions all have the potential to dramatically impact the markets. In an environment this fluid, staying diligent, well-informed, and focused on long-term goals becomes even more critical.

Wednesday’s Consumer Price Index (CPI) report offered investors another dose of good news on inflation. For the fourth month in a row, data from the Bureau of Labor Statistics came in cooler than expected, adding to a growing sense that price pressures are easing. Consumer prices rose just 2.4% over the prior 12 months, while core CPI—which excludes volatile food and energy categories—increased only 0.1% from April.

Markets welcomed the news, interpreting the soft inflation print as a sign that the Federal Reserve may be nearing the end of its tightening cycle. The report added to growing confidence that the Fed could soon shift its focus from fighting inflation to supporting broader economic stability.

While recent data has tempered fears of a tariff-driven inflationary resurgence, pricing pressures haven’t disappeared. Grocery prices rose 0.3% in May after declining in April, and several major retailers—including Walmart and Target—have cautioned that higher input costs may soon be passed on to consumers. Automakers like Ford and Subaru have echoed similar concerns.

Moreover, Middle East developments have the potential to overshadow domestic economic developments, particularly if the allies of the warring parties become directly involved. Should that occur, Mr. Market could have to contend with a new threat – one with far greater potential consequences than those he has successfully navigated thus far.

That’s all for now. Have a great weekend and invest wisely my friends.