March 14, 2026 Market Update

Market Recap: Geopolitics and the Yield Tug-of-War

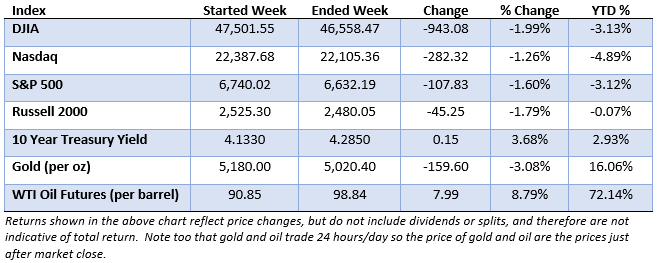

U.S. equity markets remained on edge this week as the ongoing conflict in the Middle East led to choppy trading sessions, where intraday rallies were often met with late-day reversals. While defense and energy stocks provided a partial buffer, broader indexes struggled as investors weighed the risk of a sustained energy shock against a backdrop of otherwise solid domestic growth.

In the bond market, the flight-to-safety trade has been uncharacteristically muted. Treasury yields finished the week modestly higher as investors priced in the risk that “energy-push” inflation could force the Federal Reserve to hold interest rates steady longer than previously anticipated.

As we move through the final weeks of the quarter, the balance between geopolitical risk and economic resilience remains delicate. While war risk is currently the most visible driver of price action, the underlying health of the U.S. consumer and continued gains in corporate productivity suggest the market’s primary trend remains intact.

Market Performance

Market Commentary: The Quiet Storm in Private Assets

While the Iran conflict is capturing headlines on Wall Street, a storm may be brewing beneath the surface in private asset markets. For several years, private equity and private credit have enjoyed a “golden era” of expansion fueled by exceptionally low interest rates. As we move deeper into 2026, however, cracks are beginning to show.

The concern lies in the true health of private credit. While headline default rates appear stable, they may mask a growing “shadow default” environment. New data this week suggests the true default rate could be closer to 5% when “extend and pretend” accommodations by lenders are taken into account.

Private assets are often marketed as high-yield, low-volatility investments, but that stability is frequently a byproduct of infrequent valuations rather than reduced risk. Recent developments serve as a reminder that there is no free lunch on Wall Street. While the risks remain contained for now, our focus remains on liquid public markets where Mr. Market provides daily accountability.

In Case You Missed It: The Hormuz Bottleneck

Roughly 20 million barrels of oil pass through the Strait of Hormuz each day, accounting for nearly 20% of global oil consumption. To put that in perspective, the International Energy Agency’s recent “historic” release of 400 million barrels, the largest coordinated release in history, would only offset about 20 days of a complete Hormuz shutdown.