March 28, 2026 Market Update

Market Recap

Stocks rallied Monday on optimism that tensions in Iran could de-escalate. Those gains were surrendered by midweek, with the S&P 500 falling below its 200-day moving average for the first time in over 200 sessions. While the energy sector has remained a bright spot amid supply concerns in the Strait of Hormuz, the broader market is contending with the combined pressures of geopolitical risk and persistent inflation.

In the bond market, the break from traditional safe-haven behavior has become even more pronounced. Concerns over the national debt and the inflationary impact of $110-per-barrel oil have led bond traders to demand higher yields across the curve. It seems the market is no longer counting on the Fed to push rates lower but rather expecting the cost of borrowing to remain elevated.

As we close out the first quarter, investors continue rotating away from rate-sensitive growth stocks toward sectors more insulated from higher borrowing costs. While corporate earnings have provided a solid anchor thus far, the outlook for the second quarter will depend on whether they can continue to outpace rising energy and financing costs.

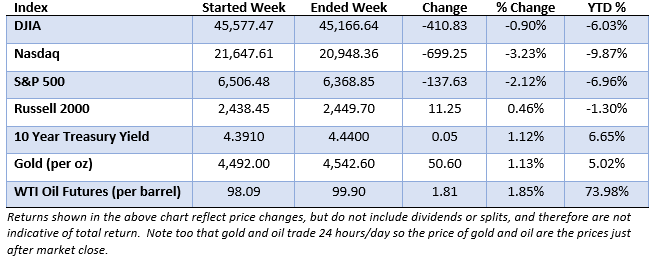

Market Performance

Market Commentary: The Cost of Conflict

An already strained federal budget—now exceeding $39 trillion—faces additional pressure this week from the costly and uncertain situation in Iran. While the market’s immediate focus has been on energy prices and supply chains, the longer-term implications for the federal deficit are becoming harder to ignore.

Early estimates suggest that the first few weeks of the conflict have already cost upwards of $25 billion in unbudgeted military expenditures. This comes at a time when the Congressional Budget Office was already projecting a $1.9 trillion deficit for fiscal year 2026. Layering the costs of a potential prolonged engagement on top of existing commitments and rising interest expenses leaves less room for budgetary maneuvering.

For Mr. Market, the concern is not just the price of the war itself, but how it is financed. Higher deficit spending typically requires the Treasury to issue more bonds. If the market becomes saturated with new debt while inflation is proving sticky, bond traders can be expected to demand higher yields to compensate for the risk. This creates a feedback loop where higher interest costs further expand the deficit, potentially limiting the Federal Reserve's ability to lower rates even if the economy starts to cool.

We continue to believe the primary trend in the U.S. economy remains one of resilience. However, the combination of geopolitical conflict and an expanding debt burden lends additional credibility to the “higher for longer” interest rate narrative.

In Case You Missed It

For the first time in history, the U.S. is now spending more on interest payments to service the national debt than it spends on its entire national defense budget. If this continues, it could have meaningful implications for fiscal policy and national security as well.