September 13, 2025 Market Update

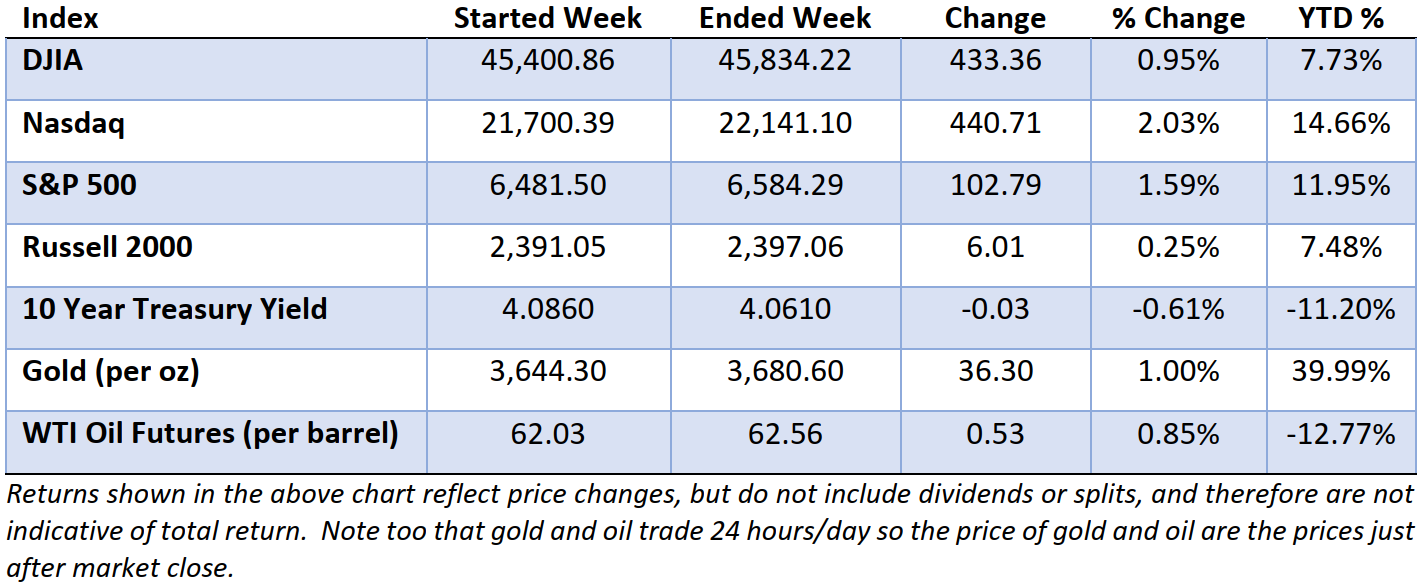

Stocks traded higher this week as investors weighed softer labor market data against still-elevated inflation. A weak August jobs report showing just 22,000 new positions, along with an uptick in jobless claims, reinforced expectations that the economy is slowing. That helped offset concerns about tariffs and consumer prices, with the S&P 500 and other major indexes notching fresh highs.

In the bond market, Treasury yields moved lower as traders reacted to the softer economic data. The 10-year yield briefly dipped below 4% following the jobs report, while credit markets remained steady. Gold also attracted flows, pushing near record highs, as investors sought protection against both slowing growth and lingering inflation risk.

The week’s moves reflect Mr. Market’s attempt to balance expectations of easier financial conditions with concern that the economy is losing momentum. For now, investors seem comfortable letting the two narratives co-exist, but the outlook remains murky.

Inflation data published this week suggests tariff hikes have not led to a dramatic rise in prices - at least not yet. The producer price index, which tracks prices manufacturers pay for inputs, ticked down 0.1% in August after a 0.7% rise in July. And although the Consumer Price Index (CPI) rose 0.4%, above market expectations, the more influential core CPI, which excludes volatile food and energy prices, also rose by 0.3% in line with forecasts.

There are several reasons tariffs haven’t yet triggered widespread inflation so far. Some companies have absorbed added costs rather than passing them on to consumers. Others stockpiled goods before tariffs took effect or shifted to suppliers in countries with lower tariff rates. Tariff effects also tend to build gradually, working their way through supply chains over time, and so we may see a greater impact as early as next month.

Until then, last week’s inflation data and recent signs of a cooling jobs market suggest the Federal Reserve is likely to cut rates at its meeting next week. The key question is whether the cut will be a quarter-point move the markets expect, or a larger half-point reduction aimed at reassuring investors and quieting critics.

That’s all for now. Have a great weekend and invest wisely my friends.